Contact Debt Payoff Planner & Tracker Customer Service

Email Support directly

Chat with our AppContacter AI Support

Why should I report an Issue with Debt Payoff Planner & Tracker?

- AppContacter will directly Email your issue/feedback to an apps's customer service once you report an issue and with lots of issues reported, companies will definitely listen to you.

- Pulling issues faced by users like you is a good way to draw attention of OxbowSoft LLC to your problem using the strength of crowds.

- Importantly, customers can learn from other customers in case the issue is a common problem that has been solved before.

|

Debt Payoff Planner & Tracker Customer Insights

1. If you consolidate debts onto a different credit card, for example for a lower interest rate, for a debt consolidation loan, it reads whatever you "paid off" as an amount that's available to throw at everything else.

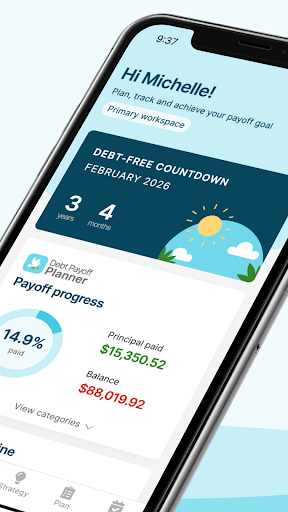

2. Perhaps a savvy developer of this app will see the benefits of it.I love this app!! I have all my debts listed and have put a snowball option on them, that shows me that I will be out of debt in 8 years ( including my house)! I never could figure out how to calculate that on my own.

3. So it can't accurately calculate the total cost or suggest the most optimized payment plan.This app is great!!!! Highly recommend for those of us trying to go through a plan to get debt paid off.

4. However, when I make a payment it adds what I had available to pay to the next debt for the same month! IE, I have one card I paid $699 on and another was for the minimum payment.

5. Once you understand the issue, it's easy enough to work around though.I love that this is simple and can follow Dave Ramsey's debt snowball.

6. And entering new payments made is a breeze, I feel like I'm getting somewhere! I get weekly emails showing how much I have paid during that week and it's nice to see that amount because I never tracked that before.

7. But there is also a free version!This app is highly beneficial for managing simple interest debts, like car loans, credit cards, and personal loans.

8. Mortgage payments often involve complex amortization schedules, where a significant portion of the interest is paid upfront.

9. Will update rating with reply / fix.The 'snowball effect' has been a proven debt elimination technique for decades.

10. I don't want to delete the old debt--like I have done previously - - because then I lose the proof of how much debt I've actually paid off.

11. You can choose to either attack your debt service either by sorting from the highest APR or starting with the lowest running balance of a debt.

Steps to Troubleshoot & Fix Debt Payoff Planner & Tracker Issues

1. Fix Debt Payoff Planner & Tracker Not Working/Crashes/Errors/Unresponsive & Black/White screen:

- Restart Debt Payoff Planner & Tracker: Restarting the app will resolve most errors.

- Update the Debt Payoff Planner & Tracker App. Here is how:

- On Android goto PlayStore » Search for "Debt Payoff Planner & Tracker" » Open Debt Payoff Planner & Tracker » click "Update".

- On iPhone, goto AppStore » Your profile » Available Updates » Check for Debt Payoff Planner & Tracker » click "UPDATE".

- Clear Debt Payoff Planner & Tracker app cache: Clearing cached data will force your app to retrieve the latest data directly from Debt Payoff Planner & Tracker servers.

- On Android, goto Settings » Apps » Select "Debt Payoff Planner & Tracker" » click Storage » click "Clear Cache".

- Check Debt Payoff Planner & Tracker app permissions. If any of these permissions required to use your device's features are disenabled, Debt Payoff Planner & Tracker might not work.

- Uninstall and reinstall Debt Payoff Planner & Tracker. If nothing else has worked, completely uninstall Debt Payoff Planner & Tracker then reinstall.

- Restart your device. Last, restarting your device can often clear most problems causing Debt Payoff Planner & Tracker not working

2. Fix Debt Payoff Planner & Tracker Server issues & Internet Connection

- Check network connection: An unstable Internet will make Debt Payoff Planner & Tracker be unable to connect to it's servers. Ensure your wi-fi is working then restart app.

- Disable VPN: VPN can cause connection errors and lead to Debt Payoff Planner & Tracker not working. Make sure all VPNs are off

- Enable background data: When Background data is turned off, Debt Payoff Planner & Tracker may not be able to connect to the Internet when running in the background.